Introduction:

Walmart has long been a dominant player in the traditional “bricks & mortar” retail space. The retailing giant has about 4,600 stores in the United States and about 6,000 stores worldwide that helped it generate fiscal year 2017 revenues of $485.9 billion. However, this retailing “Death Star” has a weakness as technological changes and innovations in its industry represent both an opportunity and a threat. The biggest threat to Walmart is the consumer preference shift from traditional in-store purchases to on-line digital channels. E-commerce is a small piece of the retail pie currently (roughly 10.4% of all retail sales in 2015), but it is growing at a pace that is much faster than growth at bricks and mortar locations. If Walmart does not evolve to defend its dominant market position, the company will erode (see Montgomery Ward, Woolworths, K-Mart, Sears) allowing other industry competitors to capitalize.

Previous disruptions in the retail space have not been kind to dominant players. Sears was able to overtake dominant retailing incumbent Montgomery Ward in the 1950’s by aggressively investing into suburbs (which was a new phenomenon for the time), while Montgomery Ward skittishly hoarded cash in anticipation of another great depression [1].

Walmart is not willing to be a Montgomery Ward in this scenario as the company became aware of the risks of e-commerce underinvestment and complacency. However, e-commerce giant Amazon is more than willing to be Sears in this example by over-investing in the more recent retail business model (e-commerce). Furthermore, Amazon recently encroached into Walmart’s home turf (i.e. physical locations) by purchasing Whole Foods for $13.7 billion. This high profile acquisition signaled to Walmart and the rest of the retail industry that Amazon is willing to take unanticipated bets to develop a competitive advantage across multiple channels.

Walmart certainly has a challenging road ahead if it wishes to catch Amazon in overall e-commerce sales but it is finally competing effectively. Although the company does not break out specific e-commerce dollars, it stated that its e-commerce sales had increased 64% domestically in the first quarter of 2017. Consider that Amazon generated $136 billion in annual sales during 2016, which accounted for half of all online shopping in the United States [2].

“With approximately 160 million items for sale, Amazon has become the go-to outlet for anything. In comparison, Walmart.com sells “only” 15 million items — and just 2 million of them are available for the free two-day shipping. It’s no wonder 52% of online shoppers start their search on Amazon, according IHL Group.” [3]

Walmart will not be able to overtake Amazon’s position as the dominant e-commerce player in the near future, but the company is positioning itself to remain competitive.

Walmart’s Main Strategic Risks in E-Commerce

Walmart’s annual 2017 10-K filing (a comprehensive summary of financial performance) details the strategic risks that the company faces. As mentioned previously, Walmart is aware of the risks of e-commerce underinvestment and complacency. Consumer preferences are shifting to shopping online and mobile platforms.

Failure to grow our e-commerce business through the integration of physical and digital retail or otherwise, and the cost of our increasing e-commerce investments, may materially adversely affect our market position, net sales and financial performance [4].

Many companies fail to adequately capitalize on the shift in consumer preferences (e.g. Smith Corona, Blockbuster, Kodak), while other firms are able to successfully capitalize (e.g. Intel, Apple). Unsuccessful companies either refuse to risk capital, lack the vision, or lack the execution competency to produce the new products and/or technologies necessary to maintain success. With that being said, Walmart plans to increase its investments in e-commerce and technology, while moderating the number of new store openings.

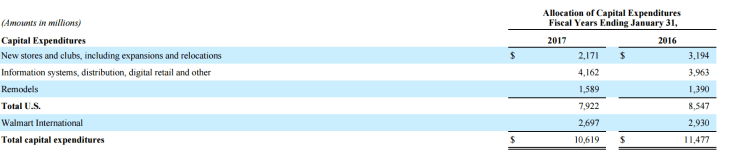

Figure 1. [4]

Figure 1. [4]

Walmart’s capital expenditures back up its strategy. Observe that a $1.023 billion reduction in new stores and clubs dove-tails with a $199 million dollar increase in already impressive expenditures related to information systems, distribution and digital retail ($4.162 billion line item).

Walmart recently divested itself of its Walmart Express brand which contributed to the reduction in new store capital expenditures. These convenience store sized locations were originally conceived in 2011 to compete in the price conscious dollar store segment. Dollar General (a digitally un-savvy competitor) purchased 41 Walmart Express stores and plans to rebrand them under the Dollar General moniker. In an age of stalled wage growth, Walmart is experiencing pricing pressure from both Dollar General and Family Dollar for the most price conscious consumers.

The bottom line is that Walmart has to walk a fine line in the implementation of its e-commerce strategy. On the one-hand, the company may not be successful in implementing and integrating its physical and digital retail channels. As of late the company has been criticized for “overpaying” for growth in regards to its acquisitions. If its e-commerce acquisitions underperform or sustain large losses, this can harm Walmart’s market position and financial performance.

On the other hand, if the company is “too successful” with their e-commerce strategy, the company runs the risk of lowering physical store traffic which could also adversely impact in-store economics. The company seems to be facing a “dammed if you don’t, damned if you do” conundrum.

“The challenge for Walmart, and for all other retailers in the e-commerce era, is to protect both sales and profits. But these goals nay be mutually exclusive. Retailers face pressure to offer both free shipping and competitive prices, which generally makes selling a product online less profitable than doing so in existing stores. To expand sales online, retailers must spend on technology, which squeezes margins further. Making matters even worse, retailers are often not gaining new customers but simply selling the same item to the same person online for less profit. ‘You pour from one bucket into a less profitable bucket,’ explains Simeon Gutman of Morgan Stanley.” [5]

Backend E-Commerce Acquisitions

Walmart’s initial e-commerce forays focused on acquiring companies that helped bolster its prowess in backend technologies. This approach was a departure from the company’s traditional “build rather than buy” philosophy which helped it obtain and retain technological competitive advantages in its supply chain processes. Its research division @WalmartLabs, augmented its e-commerce war chest by making multiple purchases in the first half of the decade. “Between 2011 and 2014, Walmart acquired 15 small companies tied in some way to e-commerce. The other thing most of them had in common was that they were selling for a bargain after failing to attract a new round of venture funding.” [6]

For example, in 2013 @WalmartLabs purchased a company named Inkiru for its predictive analytics technology to target customers in marketing campaigns. The company purchased Kosmix in 2011 to revamp its Walmart.com search capabilities; a project known as Polaris. Site optimization start-up Torbit was purchased in 2013 to optimize page loading of its e-commerce sites. The acquired technology compresses files to an optimum size based upon display by phones, tablets or desktops. The company also purchased Adchemy for its strong pool of data scientists and PhDs who have specialized knowledge in the areas of ad technology and search engine optimization (SEO).

As an aside, “CEO Murthy Nukala and four top executives all got payouts of between $1.5 million and $2 million in the deal” while employees who held common stock saw their holdings become worthless [7].

The point of these acquisitions along with others of similar characteristics, was an attempt to grow e-commerce sales organically.

The Acquisition of Marc Lore and Jet.com

Walmart learned that it is both difficult and time consuming for a firm to obtain organic growth intrinsically. When asked of his biggest regret at the helm of the company, former CEO Mike Duke who held the position from 2009 to 2013 said that the company should have moved faster to expand in e-commerce. One could draw the conclusion that Walmart either believed that growth in e-commerce would shift too much volume from bread and butter physical stores or that Amazon’s rise to e-tail prominence was not a significant threat to its dominant market position.

“When I look back, I wish we had moved faster. We’ve proven ourselves to be successful in many areas, and I simply wonder why we didn’t move more quickly. This is especially true for e-commerce. Right now we’re making tremendous progress, and the business is moving, but we should have moved faster to expand this area.” – Former Walmart CEO Mike Duke [8]

As Walmart’s sales growth continued its trend downward, new CEO Doug McMillon was tapped in 2014 to implement a new e-commerce, digital and technology focused strategy. In fact, for the first time since Walmart became a publicly traded company in 1970, annual sales shrank for the first time in 2015. McMillon was asked why did it take so long for Walmart to get into e-commerce and if the profitability of their original model affected its urgency to change. McMillon responded.

“We wish we had been more aggressive early on, no doubt. In some ways we experienced what Clay Christensen calls the ‘innovator’s dilemma.’ We hired talent, invested, and just kind of meandered along rather than hammering down, being aggressive, and making it a must-win aspect of our business. That’s partly because we had a bird in hand. We knew that if we continued to open Walmart Supercenters, they would do well.” – Walmart CEO Doug McMillon [9]

McMillion, true to his mandate, made a splash by acquiring online retailer Jet.com for 3.3 billion in cash and stock. The deal is reported to be the largest ever purchase of a U.S. e-commerce startup [10]. There were multiple reasons stated by the company for making a splashy purchase of this nature. However, the crown jewel of the acquisition was the procurement of e-commerce wunderkind Marc Lore who was immediately tapped to head both Jet.com and Walmart.com.

Marc Lore established his digital retailing bona fides by founding Quidisi. The start up was known for its diapers.com and soap.com sites amongst others. Quidisi was sold to Amazon in 2010 for $550 million. The purchase of Quidisi at the time was an attempt by Amazon to stifle competition.

“Amazon was slashing the price on diapers on its own site, putting pressure on Quidsi’s margins and making outside investors hesitant to put in more money. Furthermore, Amazon promised to keep dropping prices if Quidsi sold to Wal-Mart.” [15]

Lore stayed at Amazon for two years and then left to ponder his next move. Subsequently, in 2014 Lore founded Jet.com based upon the premise of charging members a yearly fee, encouraging consumers to buy in bulk and incentivizing consumers to purchase items from the same distribution center to lower product prices. On the strength of his name and new business model, Lore was able to raise $500 million in investment capital on this venture. Lore earned $243.9 million in 2016 making him the highest compensated CEO in the United States after the sale. Expect Lore to be at Walmart for at least five years, as he will lose substantial compensation if he exits beforehand.

Walmart previously missed out on buying Quidisi in 2010 as both Walgreens and Amazon were in a bidding war for Lore’s e-commerce property. Walmart decided with the Jet.com acquisition that they were not going to lose an opportunity to buy Marc Lore’s services again.

How Will Walmart Benefit from Jet.com?

In just one year of operation, Jet.com scaled up to 12 million different products and reached a run-rate of $1 billion in gross merchandise value [11]. With this acquisition, Walmart is buying additional diversity of online product offerings. The brands that Jet.com offers are those that appeal to consumers that reside outside of Walmart’s more suburban, rural, older cost conscious demographic. Jet.com’s brand positioning is targeted to younger, “urban”, millennials who constitute a faster growing demographic than the demographic that Walmart has traditionally attracted. Walmart plans to keep the Jet.com brand identity separate from Walmart.com. Jet.com has relationships with more upscale brands that may not want to sell their products on Walmart.com. Additionally, this brand separation helps maintain Jet’s appeal to higher income consumers.

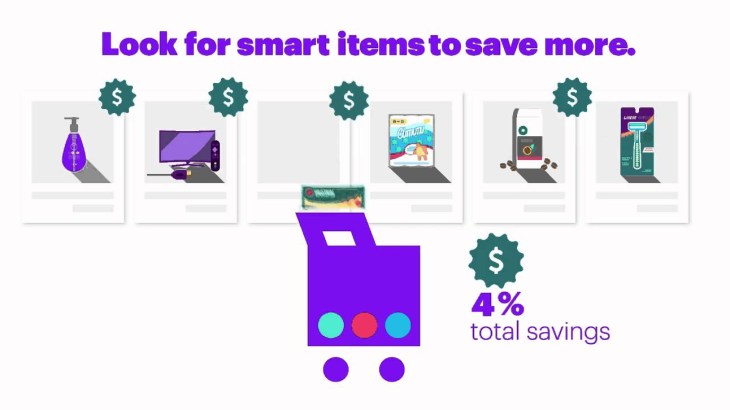

According to CNBC, Jet.com shoppers are more likely to have $150,000 and up incomes. Additionally, only 20% of Jet.com buyers also purchased from Walmart.com in the past six months (as of August 8th, 2016) [12]. There was little overlap between the customer bases of both companies making the acquisition by Walmart highly attractive. Furthermore Jet.com’s innovative supply chain business model and focus on low prices dovetailed with Walmart’s penchant for supply chain innovation and focus on low prices. Here is how Marc Lore described the company’s novel “smart cart” business process:

“Here’s how it works: If you have two items in your cart which are both located in the same distribution center and can both fit into a single box, then you will pay one low price. If you add a third item that is located at a different distribution center and cannot be shipped in a single shot with the other two items, you will pay more. As you shop on the site, additional items that can be bundled most efficiently with your existing order are flagged as ‘smart items’ and an icon shows how much more you’ll save on your total order by buying them.”

It should be noted that Jet was experiencing a high cash burn rate prior to being acquired by Walmart. Jet.com dropped its annual $50 membership fee which caused it to lose money on every shipment. The advantage of Jet.com being acquired by a deep pocketed industry player like Walmart was to help alleviate the stress of private fund-raising for an unprofitable company [13].

Walmart has to allow Jet.com to maintain its startup, entrepreneurial culture or risk losing talent. For instance, Walmart’s conservative, southern influenced culture clashed with the office drinking, happy hour culture of Hoboken New Jersey based Jet.com. Walmart eventually reversed course and did not impose this “in-office prohibition” rule on subsequent startup acquisitions. However, the more conservative Walmart did ask Jet employees to be mindful of swearing in the office [14].

Jet.com has the potential to infuse Walmart with much needed digital innovation. This fresh perspective has the potential to add tremendous value to the organization as a whole. The “old guard” rooted in Walmart’s core business model needs to allow acquisitions to thrive instead of imposing the more conservative legacy culture. According to CEO McMillon, the core business itself must learn to become more digital.

“The people who run the older parts of our business must also become digital. We can’t have some people live in yesterday while others live in tomorrow. And given the effects of inertia, we need people to lean into the future even more than other companies might. We’re trying to move large numbers of people to change their established habits.” [9]

E-Commerce Executive Shakeup

There was an immediate shakeup in the executive ranks once the Jet.com acquisition materialized. Neil Ashe, Walmart’s global e-commerce head previously ran CBS Interactive and had been named head of technology shortly before the acquisition, was transitioned out to make room for Marc Lore. Lore will assume the title of president and CEO of e-commerce at Walmart. Lore will head not only Jet.com but also all of Walmart’s e-commerce functions. Also leaving is Michael Bender, Walmart’s global e-commerce COO.

Fernando Madiera who previously headed Walmart.com and was previously CEO of Walmart’s Latin American e-commerce business was transitioned. Mr. Madiera had just taken the Walmart.com post in 2014. Other high level executives that transitioned were Dianne Mills, senior vice president of global e-commerce human resources; and Brent Beabout, senior vice president of e-commerce supply chain. Not even Wal-Mart’s chief information officer Karenann Terrell was spared, as she left the company late February of 2017.

Key executives from Jet.com that will join Marc Lore’s new team include Scott Hilton who was previously chief revenue officer at Jet.com. Jet.com co-founder Nate Faust will become the senior vice president for U.S. eCommerce and supply chain for Walmart’s domestic operations.

The point of this game of executive musical chairs is to provide Marc Lore with the executive team he deems necessary to launch an effective attack on Amazon’s e-commerce dominance. Walmart has 3.3 billion reasons to make sure Lore feels he has the necessary team in place to win.

Walmart & Jet.com E-Commerce Timeline

- February 2016: Jet.com purchases online furniture retailer Hayneedle.com for $90 million. The move is seen as way for Jet.com to acquire revenue growth. Of note, the Hayneedle CEO (John Barker) received a parachute package worth $3.4 million while other employees saw their investment stakes effectively wiped out.

- August 2016: Walmart purchases Jet.com for $3.3 billion. The deal is reported to be the largest ever purchase of a U.S. e-commerce startup.

- January 2017: Jet.com purchases Boston based ShoeBuy for $70 million. The purchase increases Jet’s online catalogue of items substantially and will allow the same items to be sold across Walmart.com, Jet.com and Shoes.com.

- February 2017: Walmart purchases hip Michigan based outdoor retailer Moosejaw for $51 million. Moosejaw sells brands like Patagonia and North Face online and in its 10 brick and mortar stores. Moosejaw has expertise in online sales and social marketing that Walmart wishes to tap. Moosejaw and Its 350 employees will continue to exist as a standalone subsidiary.

- March 2017: Jet.com purchases women’s online clothing retailer Modcloth for $75 million. The site caters to size diversity and body positivity. The acquisition represents an attempt to appeal to a younger, hipper demographic than Walmart currently courts.

- March 2017: Walmart launches a Silicon Valley based tech incubator called Store No. 8. The initiative is named after a store where Sam Walton was known to experiment. Walmart plans to invest in businesses like a venture capitalist firm would and then grow this group of startups as a portfolio. “The incubator will partner with startups, venture capitalists and academics to promote innovation in robotics, virtual and augmented reality, machine learning and artificial intelligence, according to Wal-Mart. The goal is to have a fast-moving, separate entity to identify emerging technologies that can be developed and used across Wal-Mart.” [18]

- June 2017: Walmart purchases NYC based men’s clothing retailer Bonobos for $310 million. The brand started modestly by selling chino pants and expanded its line of offerings for sale in its own stores and in Nordstroms. “Its co-founder and chief executive, Andy Dunn, will oversee Walmart’s digital brands, which also include the independent women’s brand ModCloth.” [16] Passionate Bonobos fans have mocked the acquisition on social media snarkily asking if the popular chinos will be refitted for the average Walmart customer. Bonobos has a vertically integrated supply chain as it designs and manufactures all products in-house, which allows it to cut out middlemen costs [17]. Walmart is eager to tap founder Andy Dunn for his expertise in this area.

Peddling upscale merchandise will allow Walmart to expand its reach from low and middle income consumers to a more affluent base. As middle income consumers slowly shrink, Walmart is diversifying its customer base.

“Between 2000 and 2014, middle-class populations decreased in 203 of the 229 metropolitan areas reviewed in a Pew Research Center study. In an economically divided America, Walmart has tried to sell not only to shoppers looking for extreme discounts, but also to shoppers with higher incomes seeking higher-quality items. Walmart has been working to increase its sales to more affluent customers for years, especially in e-commerce.” [19]

Conclusion

Walmart’s e-commerce strategy appears to be reaping dividends as of the writing of this post. As mentioned earlier, Walmart stated that its e-commerce sales had increased 64% domestically in the first quarter of 2017.

For years, Walmart has dominated the retail space with its low cost/low price strategy (see my Micheal Porter post). In today’s e-commerce environment, the key is to compete on low prices and convenience, as well as appeal to diversified income groups. Only time will reveal if Walmart has the innovative capacity and leadership to overtake Amazon. The company is making bold bets in the e-commerce space and is aware of the shift in consumer preferences.

Walmart’s core business must be willing to be disrupted by its internal innovators. The current retail landscape is one of declining profits and closing stores. The organization as a whole must not be ideologically wedded to its massive assortment of physical stores while ignoring threats from outside competitors (namely Amazon).

Additionally, Walmart cannot ignore fresh retail ideas emanating from internal disrupters like Marc Lore, Andy Dunn or successful Store No. 8 startups if they materialize. The company must cross-pollinate successful ideas and quickly post-mortem and move on from unsuccessful ones. If Walmart continues to buy online growth at the expense of organic growth, then it must ensure that it does not continually overpay for growth and assets. If its e-commerce acquisitions underperform or sustain large losses, this can harm Walmart’s market position and financial performance.

For more Walmart coverage please check out Part 1, Part 2 and Part 3 of my series on Walmart’s overall technology strategy, where I address areas such as:

- Strategy for Technology Infrastructure

- Strategy for IT Capability & Staffing

- Strategy for Information Risk & Security

- Strategy for Stakeholder Requirements, Testing & Training/Support

- Project ROI and Key Success Measures

- Strategy for Data Acquisition and Impact on Business Processes

- Strategy for Social Media/Web Presence

- Strategy for Organizational Change Management, Project Strategy and Complexity

If you’re interested in Business Intelligence & Tableau check out my videos here: Anthony B. Smoak

References:

[1] Kaufman L. & Deutsch, C. Dec 29, 2000. Montgomery Ward to Close Its Doors. New York Times. http://www.nytimes.com/2000/12/29/business/montgomery-ward-to-close-its-doors.html

[2] Abrams, R., May 18 2017. Walmart, With Amazon in Its Cross Hairs, Posts E-Commerce Gains. New York Times. https://www.nytimes.com/2017/05/18/business/walmart-online-sales-jump-63-percent.html?mcubz=0

[3] Yohn, D., March 21, 2017. Walmart Won’t Stay on Top If Its Strategy Is “Copy Amazon”. Harvard Business Review. https://hbr.org/2017/03/walmart-wont-stay-on-top-if-its-strategy-is-copy-amazon

[4] Walmart STORES, INC., ANNUAL REPORT ON FORM 10-K FOR THE FISCAL YEAR ENDED JANUARY 31, 2017. http://d18rn0p25nwr6d.cloudfront.net/CIK-0000104169/c3013d40-212d-409e-bf30-5e5fd482fc2f.pdf

[5] The Economist. June 2, 2016. Walmart: Thinking outside the box. As American shoppers move online, Walmart fights to defend its dominance. http://www.economist.com/news/business/21699961-american-shoppers-move-online-walmart-fights-defend-its-dominance-thinking-outside

[6] Levy, A. April 24, 2017. Is Wal-Mart’s New E-Commerce Acquisition Strategy Any Better Than Its Old One? https://www.fool.com/investing/2017/04/24/is-wal-marts-new-e-commerce-acquisition-strategy-a.aspx

[7] Edwards, J. May 27, 2014. Some Employees Are Furious At Management Payouts In Walmart’s Big Adtech Acquisition. http://www.businessinsider.com/adchemy-stock-payouts-in-walmartlabs-acquisition-2014-5

[8] Lutz. A. Dec 12, 2012. Walmart CEO Mike Duke Shares His Biggest Regret. Business Insider. http://www.businessinsider.com/walmart-ceo-shares-his-biggest-regret-2012-12

[9] Ignatius, A. March 2017. “We Need People to Lean into the Future”. Harvard Business Review. https://hbr.org/2017/03/we-need-people-to-lean-into-the-future

[10] Nassauer, S. Nov 1, 2016. Wal-Mart E-commerce Executives Depart in Wake of Jet.com Purchase. Wall Street Journal. https://www.wsj.com/articles/wal-mart-e-commerce-executives-depart-in-wake-of-jet-com-purchase-1478038997

[11] Gustafson, K. August 8, 2016. Wal-Mart: This is why Jet.com is worth $3.3 billion. CNBC. http://www.cnbc.com/2016/08/08/wal-mart-this-is-why-jetcom-is-worth-33-billion.html?view=story

[12] CNBC Interview with Marc Lore. Aug, 9. 2016. https://www.nytimes.com/2016/08/09/business/dealbook/walmart-jet-com.html?mcubz=0

[13] Abramsaug, R. & Picker, L. August 8, 2016. Walmart Rewrites Its E-Commerce Strategy With $3.3 Billion Deal for Jet.com. New York Times. https://www.nytimes.com/2016/08/09/business/dealbook/walmart-jet-com.html?mcubz=0

[14] Baskin, B. & Nassauer, S. June 25, 2017. It’s 5 O’Clock Somewhere—Unless You’ve Been Acquired by Wal-Mart. The retailing giant bought Jet.com for $3.3 billion, then had to cope with its weekly happy hour. Wall Street Journal. https://www.wsj.com/articles/its-5-oclock-somewhereunless-youve-been-acquired-by-wal-mart-1498410840lipi=urn%3Ali%3Apage%3Ad_flagship3_feed%3Bu3d9V%2FcPTBqo%2BB0cP7nSZQ%3D%3D

[15] Levy, A. August 9, 2016. Why Wal-Mart couldn’t let Jet.com’s founder get away…again. CNBC. http://www.cnbc.com/2016/08/09/why-wal-mart-couldnt-let-jetcoms-founder-get-away-again.html

[16] de la Merced, M. June 16, 2017. Walmart to Buy Bonobos, Men’s Wear Company, for $310 Million. https://www.nytimes.com/2017/06/16/business/walmart-bonobos-merger.html?smid=li-share

[17] Sergan, E. June 19, 2017. Bonobos Founder Andy Dunn Knows You Might Be Mad At Him For Joining Walmart. Fast Company. https://www.fastcompany.com/40432313/bonobos-founder-andy-dunn-knows-you-might-be-mad-at-him-for-joining-walmart

[18] Soper, S. March 20, 2017. Wal-Mart Unveils ‘Store No. 8’ Tech Incubator in Silicon Valley Bloomberg. https://www.bloomberg.com/news/articles/2017-03-20/wal-mart-unveils-store-no-8-tech-incubator-in-silicon-valley

[19] Taylor, K. March 24, 2017. Walmart’s latest move confirms the death of the American middle class as we know it. Business Insider. http://www.businessinsider.com/walmart-invests-as-american-middle-class-shrinks-2017-3

Photo Copyright: moovstock / 123RF Stock Photo