To my surprise, one of the more popular blog posts on this site has been my excerpt from an MBA group paper drafted for a strategic management class (MGT 6125) taken back in the Spring of 2007 at the Georgia Institute of Technology.

The class was taught by the esteemed professor of strategy, Dr. Frank Rothaermel who literally wrote the book on strategic management. As part of the class our project group interviewed an executive from ADP (Mr. Greg Secord who went on to become President of ADP Canada), wrote a strategic analysis of the company and then presented our findings to the company (complete with Q&A).

Due to the aforementioned popularity of the excerpt that I authored, I have decided to post the paper in its entirety as written by me and other project members. Please keep in mind that this work was originally submitted on April 23, 2007 so please peruse the information with the proper context in mind. I must give credit where credit is due as this paper was put together by Brent Dutton, John Frazer, Jay Hornback, Kyungrok Jung, Chris Nygren, Anthony Smoak, Tom Whittingham, et.al.

Company Background

Automated Data Processing, Inc. is a company that many people have heard of but may not be fully aware of its value proposition. ADP processes payroll for 1 in 6 Americans [1]. While payroll processing is its core competency, it is not the organization’s only line of business worth highlighting. Tax filing, benefits administration and labor management are just a few of the company’s other services. The purpose of this analysis is to offer a better understanding of ADP as a company. We will offer insight into the functions that the organization performs, how they have maintained success and where they are headed as an organization.

ADP’s corporate culture and structure bolster its internal strengths and contribute to the company’s competitive advantage. In addition, expansion and integration have contributed to ADP’s unmatched growth in the industry. ADP’s business level strategies and unique competencies have also been a contributing factor in its growth. This strategic analysis offers a detailed inspection of each of these growth factors and as well as recommendations that should help foster future growth and success.

Before diving into the current state of the business and its strategy, it is important to understand the company’s past. In 1949, Henry Taub became the sole owner of what would become ADP at the age of 21 [2]. This humble beginning, managing one client’s payroll, would slowly snowball through the 1950s as more companies saw the value from payroll outsourcing. ADP expanded by absorbing “Mom and Pop” payroll processors in major U.S. cities and expanding their local clientele.

In the 1960s, ADP became a publicly traded company and continued its expansion strategy. It developed a Brokerage Services division which provided services for stock brokerages on Wall Street. The 1970s saw further domestic expansion as well as ADP’s first international office in The Netherlands. A new Dealer Services division was created to cater to the inventory and accounting needs of automobile dealers. The decade wrapped up with the creation of Claims Services, another valuable division positioned to automate insurance estimates for insurers.

The growing PC industry of the 1980s posed a serious threat to ADP as many companies could more feasibly perform ADP’s services in-house. However, ADP proved up to the challenge by turning that threat into a strength as they absorbed this new technology into their operations. The company crossed the $1 billion revenue mark in the mid-80s and found themselves in the perfect strategic position as outsourcing became trendy in the 1990s. Into the 2000s, ADP boasts 570,000+ clients, 42,000+ employees and $7 billion+ revenue as they continue to be a leader in the HR outsourcing industry.[3]

Industry Analysis

In order to analyze the industry in which ADP competes, Porter’s Five-Forces Model was applied. In the context of this model the competitive makeup of the employee services industry becomes clear.

Threat of Potential Entrants

The threat of potential entrants is relatively low as the result of significant barriers to entry. These include high switching costs for customers and large upfront capital investment for potential competitors. There is little upside to performing payroll processing correctly and significant consequences for performing it incorrectly. As a result, companies are leery of switching payroll providers, giving new entrants little chance of stealing customers from existing payroll firms and thereby limiting the size of the market for new entrants. A large initial capital investment is also needed to establish the hardware and software infrastructure needed to process high volumes of transactions efficiently and effectively. In addition, an extensive sales force needs to be in place to combat the industries largest substitute.

Substitutes

The threat of substitutes is high, and primarily revolves around the mindset of businesses wanting to process payroll themselves [4]. Some plausible reasons include not wanting to lose control of the financial books or being unaware of the cost savings associated with outsourcing functions like payroll [5]. Other substitutes include ERP software like Oracle and SAP.

On the larger scale there are two Macro-environmental forces that have an affect on the industry as a whole; the Technological and Macroeconomic environments. Technology has not only helped the industry to increase the speed in which it can process transactions, but it has also increased the reach of individual companies. For example, ADP began operations using paper and pen to process payrolls. Later they moved onto calculators, punch cards, and mainframes. The processing power of mainframes increased the number of daily transactions they could process and in turn helped to grow the business.[6]

Lastly, the Macroeconomic Environment can affect the potential of companies to attract new clients and maintain current revenue streams. During an economic downturn companies are less likely to spend capital on nonessential projects resulting in fewer new clients. Also, a reduction in a client’s workforce has a direct relationship to the amount of steady revenue received[7] because a smaller workforce equals fewer payroll transactions processed.

Strength of Buyers

The strength of the buyers in the payroll industry is proportionate to the size of the buyer, or more specifically, the number of employees the buyer has. Recently, many of ADP’s clients in the fragmented financial services industry have begun to merge and consolidate. In fact, there are 770 fewer such institutions in 2007 than there were in 2000[8]. While this consolidation has not happened yet on a large enough scale to severely impact ADP’s margins, it may do so in the near future if the trend continues.

Intensity of Rivalry

For the first forty years that ADP was in business it enjoyed very little competition in its industry. This was due mainly to the fact that ADP had developed a series of in-house competencies using complex technology such as punch card computers and later mainframes to process their customers’ transactions. Not many other companies had the expertise to handle this difficult technology efficiently and effectively. However, the advent of the personal computer and user friendly software such as PeopleSoft greatly lowered technical barriers to entry into the industry. This resulted in the advent of numerous new competitors such as Paychex, Ceridian, and Administaff. Although the payroll industry is still dominated by a few players (ADP and Paychex primarily), the PEO and BPO industries that ADP operates in feature many competitors and intense competition. This has already led to price competition and if it continues will hurt ADP’s profit margins.

SWOT Analysis: Strengths

ADP recorded a robust financial performance for the time period 2004 – 2006. Revenue has increased over the past year at the rate of 10%, operating profits 10%, net profit 29%, and cash flow 14% respectively [9]. This financial strength is the foundation for ADP’s future growth. For this industry with small margins and a high cost of acquiring new business, client retention rate is very important. ADP’s average client tenure is estimated at ten plus years, which exceeds the industry’s average [10]. This has allowed ADP to enjoy very predictable recurring revenue streams. ADP’s broad range of offerings is also a strength. These include computerized payroll, transaction processing, data communications, and IT-based business solutions [11]. ADP can offer substantial scale advantage across all its product offerings, which enables it to cater to a larger customer base. As a main player in the industry, ADP consistently processes difficult, mundane, and high-volume transactions very efficiently at a comparatively low cost. Additionally, ADP has established effective and robust business channels through a highly trained and competent sales force of more than 4000 associates; something that is very difficult for competitors to imitate. On top of that, top management succession has been extremely smooth and has caused very little disruption since the 1950s [12]. Lastly, decentralized organization makes for smoother transitions during M&A periods.

SWOT Analysis: Weaknesses

Increasing consolidation in the financial services industry has resulted in the creation of larger entities with more bargaining power. These larger players have adversely affected the margins of the company. First, for the period of 2004 – 2006, ADP’s return on average assets, investments and average equity were 4.6%, 5.1% and 18.8%respectively. This is significantly lower than corresponding industry averages of 8.4%, 10.2% and 21.6% over the same period. Weak returns indicate the inability of the management to deploy assets profitably and can adversely affect investor confidence[13].

Another weakness is their very high dependence on the U.S. market. ADP earned nearly 83.7% of its revenues from the U.S. market in 2006 [14]. The company has a presence in Europe and Canada, but the comparative revenue is smaller. A domestic concentration of revenues makes ADP vulnerable to adverse market conditions in the U.S. Further, ADP doesn’t have a scale advantage in its international market. Having a relatively small presence in international market makes ADP vulnerable to certain foreign risks – dealing with legal systems, establishing distribution channels, finding trained people for the right position, etc. Lastly, ADP has lost much of its tradition of innovation. ADP had been successful in adopting new technology and in turning technological threats into opportunities. ADP was the first to introduce early computer machines into payroll systems. With the threat of mini-computers and PCs in the 1980s, ADP saw this new technology’s potential for company growth and integrated it successfully [15]. But, as the company grew, it became understandably more conservative in its pursuit of new technologies. As a result, ADP will now typically wait for a new technology to be commercially proven before it will consider adoption. Because the most likely disruptive force in ADP’s industry will come in the form of a new technology, ADP’s lack of product innovation and conservative approach to new technology could prove to be a weakness.

SWOT Analysis: Opportunities

ADP still has room for growth in the Domestic Markets. Current estimates place the small business sector at 10 million companies and of that, ADP only does business with 9% of this set [16]. Similar opportunities exist in the large business sector where ADP services 26% of employees [17]. ADP should also look to up-sale current customers who do not outsource their entire HR department. Finally, ADP needs to continue to evaluate foreign markets like India. As India’s citizens grow their annual salaries, so do the opportunities for ADP to offer their outsourcing products.

SWOT Analysis: Threats

The two primary threats that ADP faces are disruptive technology and both potential and current competitors. Up to this point, ADP has been able to adapt to changes in the technological environment. This includes adapting to the introduction of PCs by offering software solutions that resided at clients’ sites [18]. Potential competitors include companies like IBM, who have large amounts of capital and come from industries with lower expected ROI. Within ADP’s own industry, competitors like Paychex are growing rapidly. Today, Paychex focuses mainly on small size businesses [19]. However, as they continue to grow so does the potential that they will bleed into ADP’s market and become more direct competitors.

Competitive Position

Throughout its corporate history ADP has managed to positively differentiate itself relative to its competitors and achieve and maintain superior profitability compared to the industry average [20]. This is indicative of a sustained competitive advantage. In order to understand how ADP has differentiated itself through its competitive advantage, it is necessary to examine the sources of their advantage and understand how they continually reinforce each other. Though there are certainly numerous factors that have contributed to ADP’s success, probably the three key attributes that fuel its competitive advantage are the firm’s brand equity and reputation, its powerful sales force, and its ability to retain clients.

ADP was founded over fifty years ago and is the longest running payroll/HR company in its industry. This is actually quite a feat considering their industry and the types of services that they provide to their clients. By managing such highly visible, though mundane functions such as payroll, benefits and retirement services, ADP is put in an uncompromising position. If the company performs its job well, no one notices. But if it errs in its performance, many will notice and will likely exhibit a highly (negative) emotional response toward ADP. Therefore, in order to prosper in this “no fail” environment, ADP must continually prove to its clients and potential customers that it is extremely reliable and consistently good. Based on the fact that they have been steadily growing over the past fifty years, clearly ADP has managed to remain reliable. In doing so, ADP has built up major brand equity and is highly regarded in the industry. This solid reputation for consistent performance is the first source of their competitive advantage. The result of ADP’s strong brand and reputation come is its high revenues and solid profits. This puts ADP in a healthy financial position, and ultimately allows them to support a large sales force of over 4000 sales associates [21]. ADP’s large sales force is their second source of competitive advantage.

It is their sales force that allows ADP to have a personal presence in every single deal that they pursue [22] (uncommon in today’s world of web and phone based sales). This results in new business growth beyond that of their competitors and a greater brand equity, reinforcing their first source of competitive advantage. Further, in order to effectively compete with ADP, competitors must be able to finance a large sales force of their own. Not many firms have the capital to do this, which provides a high barrier to entry in ADP’s industry. Additionally, ADP uses its sales force to continually serve the clients that it already has. This ensures that there is always someone to personally handle any issues or meet any requirements that a client may have. Due to this highly responsive and effective service provided to its clients, ADP has enjoyed an average client tenure of over ten years [23]. It is this high client retention level that is their third source of competitive advantage.

Keeping the clients that it earns for ten years or more provides a number of benefits to ADP beyond simple client familiarity. First, it prevents market share erosion – once a client goes with ADP, they are very unlikely to leave for a competing firm. Second, it provides an industry barrier to entry because with fewer potential companies to target (since ADP has walled off a large number of clients already), competitors are less likely to enter the industry. Third, and probably most important, ADP’s lengthy client tenure translates into over 90% of its revenues being recurring. This puts ADP in an extremely healthy position financially because not only does it have guaranteed revenue streams, but it also allows the company to plan financial moves years in advance with an extremely high degree of accuracy. ADP can then use its revenue streams to fund its sales force, which in turn strengthens its brand equity, which in turn helps gain and retain clients.

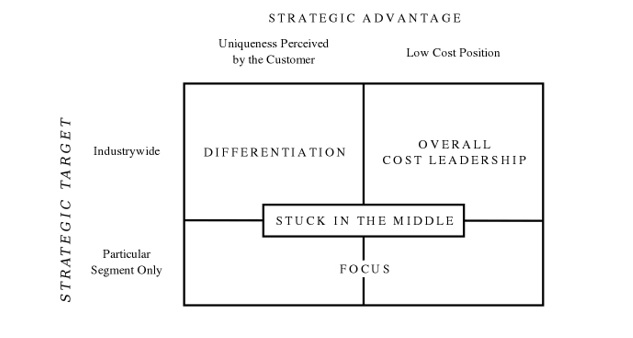

ADP’s reinforcing sources of competitive advantage are very powerful and continue to build upon themselves. These competitive advantages are very difficult to imitate. This has ultimately allowed ADP to differentiate itself in the industry (See Appendix A). As a result of this differentiation, ADP can charge a premium on its services. This premium is very important in terms of profitability since ADP operates in a relatively low margin industry.

Market Segmentation

ADP has divided their offerings into two main divisions. The primary division is their Employer Services Division that covers all HR offerings as well as the corporate tax services. Employer Services is broken down by company size into three segments for sales purposes. The smallest segment (Small Business Servies) includes all companies with 50 employees or less and represents $0.9 billion in annual revenue [24]. The middle segment (Major Account Services) includes companies that range from 50 employees to less than 1000 employees and represents $1.7 billion in annual revenue [25].

The final segment (National Account Services) is the large employer segment, made up of companies with more than 1000 employees. The National Account Services segment represents $1.6 billion in annual revenue. ADP has strong market penetration in the Major and National Account segments but is currently dealing with slowed growth within these segments. ADP must look to expand into the Small Business segment to grow their market share. This may prove difficult because smaller companies are very price conscious and ADP charges a premium rate for their services. To expand into this price competitive market ADP will have to demonstrate to these companies that it is less costly to outsource payroll and other functions to ADP than it is to do those functions in-house.

Additional revenues in the Employer Services division are gained through ADP’s total source PEO service and product oriented business units. The product oriented business units are comprised of tax, retirement, and pre-employment services. While the PEO service represents only $0.7 billion in annual revenue we feel that this is another growth segment that ADP can focus on. The entire employer services division provided ADP with $5.7 billion in annual revenue in FY 2006.

ADP’s second division is the Dealer Services division which provides multi-purpose software packages for auto dealers. The Dealer Services market is also split into three market segments. The largest segment of the dealer services market is the Domestic Auto Dealers. The second segment represents International Auto Dealers. Finally, ADP’s third segment is the Recreational Vehicle and Commercial Truck Segment. Altogether, Dealer services has 25,500 customers representing $1.6 billion in annual revenues.

Business Level Strategy

ADP has three main business level strategies. The most important strategy focuses on using “solid time tested operating principles”[26]. By utilizing proven operational methods and products for all services ADP is able to provide solid, consistent performance in all market segments. This reliable consistency is especially critical given the nature of ADP’s services. Mistakes in processes such as payroll are highly visible to employees and employers. If ADP were not able to deliver this consistent service their clients would leave in droves. Thanks to ADP’s reliable operations and core knowledge of the transaction services business they can boast over a 90% client retention rate.

The second main business strategy stems from ADP’s decentralized corporate structure. By making decisions at the lower levels of management, ADP is able to deliver superior service to their clients. The flat corporate structure allows for flexibility and incremental improvements in services that are unhindered by bureaucratic obstacles. Because of this, ADP is able to quickly respond to and fill customer needs faster than their competitors. This strategy will become more important as ADP begins to expand into the Small Business segment where customers will have more specialized demands.

The final business level strategy is the direct sales force employed at ADP. By maintaining a sales force of over 4,000 dedicated field representatives ADP is able to include a personal touch on almost every business transaction. As mentioned earlier in the paper ADP’s sales force is seen as a competitive advantage by itself. By saturating the marketplace with well trained, capable sales personnel ADP is able to nurture and capitalize on personal relationships. While this is a competitive advantage it is also extremely costly. The high costs associated with the sales force could be ADP’s greatest weakness in targeting the lower margin Small Business market. Because of this higher cost, ADP has begun to experiment with telephone and web-based sales pitches to target the Small Business market. Using these less expensive marketing channels will allow ADP to quickly and inexpensively contact a greater number of small businesses and hopefully increase their client base within this market.

Mergers and Acquisitions

ADP has become highly successful in its strategy of pursuing growth via horizontal integration. Although current CEO Gary Butler has maintained that ADP has no interest in “large, dilutive, multiyear acquisitions” [27], the company actively acquires smaller industry competitors. Acquisitions give ADP the opportunity to grow inorganically, increase its product offerings, acquire technology and reduce the level of rivalry in its industry.

A perfect execution of this strategy can be seen in its January 2003 acquisition of Probusiness. Probusiness was a much smaller California based provider of payroll and human resources services. Before the acquisition, Probusiness cited eight large competitors who had an interest in acquiring them. An acquisition of Probusiness would give a larger company an opportunity to expand its share of the payroll business [28]. Amongst those eight competitors were notable companies such as International Business Machines Inc. (IBM), Microsoft Corp. and Electronic Data Systems Corp. (EDS) [13]. True to form, ADP decided to react and proceeded to acquire Probusiness. The acquisition effectively prevented large competitors from acquiring approximately 600 new payroll clients in the larger employer space and reduced future competition.

The Probusiness acquisition was also a boon to the company in the fact that it offered ADP advanced payroll processing technology. Probusiness utilized PC based payroll processing as opposed to ADP’s more mainframe based technology [13].

A key acquisition for ADP in terms of increasing its global footprint was the December 2005 acquisition of U.K. based Kerridge Computer. This particular acquisition was significant in the fact that it increased ADP’s Dealer Management Services (DMS) presence from fourteen countries to over forty one [29].

ADP along with its main DMS competitors in the European market, Reynolds & Reynolds and SAP, began to realize the significant growth opportunities for the region. The European market for DMS, unlike the United States market, is much more fragmented which means there are more opportunities for a larger player to standardize product offerings [30]. In 2003 the European Union lifted rules that had previously banned franchised car dealers from selling rival brands [15]. Demand for pan-European systems to help multi-brand dealers manage their stores, sometimes in multiple countries and in various languages increased dramatically [15]. ADP shrewdly realized that many smaller DMS providers would not be able to meet this demand and acquired Kerridge to bolster its position.

Strategically, the Kerridge acquisition has allowed ADP to have first mover advantage over its main competitors with respect to China. New vehicle sales growth in Asia is expected to be at 25.3% by the year 2011 [31]. By becoming a first mover in the region, ADP will have the opportunity to lock customers into its technology since it currently has a 96% client retention rate16. ADP will also have the opportunity to create high switching costs for its customers and make it difficult for rivals to take its customers.

Other recent acquisitions by ADP include Taxware, which brings tax-content and compliance solutions to the table; VirtualEdge, which offers tools for recruiting; Employease, which develops Web-based HR and benefits applications; and Mintax, which provides tools for corporate tax incentives [32].” All of these acquisitions represent small fast growing companies with complimentary products and services. These products and services can be incorporated in ADP’s vast distribution network and provide potential bundling, cross-selling, or up-selling opportunities with ADP’s current offerings.

Culture, Structure, and Control Systems

Top management at ADP plays an important role in maintaining and advancing the culture created by its founders. The promotion of the core values by top managers sets the tone for the entire organization. ADP stresses the following three core values: 1.) treat everyone with honesty, fairness, and respect; 2.) conduct business with the highest level of integrity; 3.) open, informal communications, hard work, and prudent financial management [33]. Adhering to these values has created a culture of prudent risk taking, continuous improvement, and promotion from within based on ability. As a company that built its core business around delivering first class applications to its client base, maintaining an environment where employees advance their careers based on their ability to improve services is essential because better services lead to higher client satisfaction. Client satisfaction is the most important metric for client retention, and retention is imperative for a mature company with 46,000 employees and 570,000 clients [34].

Creating incentives for employees to adopt and adapt new technologies will be paramount as ADP begins to embrace the software-as-a-service platform. Collaboration and incremental innovation occur naturally at ADP as a byproduct of its relatively flat, multidivisional organizational structure. As a result managing change during a paradigm shift should be relatively painless for the company. ADP’s flat corporate structure meshes well with its core values and business objectives. ADP avoids excess management layers in favor of decentralized authority and empowered product teams. These empowered associates respond well to this structure as it gives them a better sense of their mission, their accomplishments, and their accountability. Ultimately this leads to happier employees and better service levels [35]. Better service levels lead to longer relationships with ADP, expanded service offerings and more references to other companies who use ADP’s products and services [36].

As mentioned above, ADP advocates incremental innovation and relies heavily on outsiders to produce new products or platforms. Once the benefits of the technology are well known, ADP leverages the new technology to enhance its product offerings. This strategy has fewer risks and lower costs as opposed to investing directly in R&D and innovating internally. Streamlined implementations with aggressive timelines – most are completed in less than one year [37] – allow ADP to catch up quickly and capitalize on the advances along with the first movers. Dedicated cross-functional product teams “live with” the product implementation from its initial project management stages to the final testing and quality assurance phase. These experienced and focused teams deliver new products in half the time of most competitors. ADP also has strategic control systems in place to ensure products continue to meet their high quality standards. The Product Marketing Council and Product Steering Committee meet regularly to evaluate the quality of their products and services in terms of how effectively they meet the client’s business needs and how reliably the applications actually perform. Managers at these meetings also examine industry trends and external product innovations and assess the need to change platforms or introduce new products to ADP.

Recommendations

Over the past fifty years, ADP has a history of planned long-term growth. In the past twelve months, ADP divested their Claims and Brokerage Service businesses. ADP has made a clear strategic focus on the Employer and Dealer Service businesses, part of the new “Fit and Focused” ADP brand. Below are two strategic recommendations for ADP that mesh well with its strengths and the opportunities present in the industry.

Inorganic Growth in Employer Services

ADP has been very successful in matching organic growth with inorganic growth through mergers and acquisitions. Currently, the Professional Employer Organization, or PEO segment of the Employer Services business, is highly fragmented with solid expected growth. In some domestic PEO markets, ADP will be able to grow their presence with their existing ADP Total Source package. New regulations make California a prime market to expand with PEO services [38].

However, the PEO market as a whole is highly fragmented. Currently, over 700 firms provide PEO services to small businesses throughout the US. The overall market penetration of PEO services is about 2.5% with annual growth of about 20%. ADP is in a unique position to grow in this segment because ADP has the largest capital structure (see Appendix B) [39]. ADP could greatly accelerate their growth in this promising market through continued mergers and acquisitions.

Dealer Services in the Booming Chinese Auto Market

As mentioned in latter portion of the Mergers and Acquisitions section, ADP acquired Kerridge Computer which expanded the Dealer Services business internationally. The Dealer Management Service, or DMS, industry will continue to have steady growth in North America and Western Europe. The largest, long-term growth potential, however, is in the Chinese automotive market. The growing economy and shift from institutional vehicle purchases to individual purchases are the primary reasons for a need to increase ADP’s DMS presence in China.

“China’s auto demand is expected to rise to 10 million in 2010, second only to North America,” says Zhang Xiaoqiang, Vice Minister of the State Development and Reform Commission [40].

Currently, the automotive market in China is around 2 million vehicles per year. Thus the projections of the Chinese government equate to 20-30% growth over the next several years [41].

The automotive growth in China also lends to growth in the DMS industry because the Chinese auto market is switching from an institutional sellers market to an individual consumer buyers market [42]. The switch in customer base will put an increased need for dealerships to provide more personalized and generally better customer service. DMS systems can help dealerships manage their business more effectively while focusing more time on building their customer base and nurturing customer relationships. ADP clearly has a focus on the growing Chinese automotive market with its recent announcement with BMW of China [43]. Building on that, ADP needs to continue to focus resources and energy on the great opportunity China’s automotive market provides.

Endnotes

[1] http://www.adp.com/employer_services_overview.asp?iid=EFI0483

[2] Kanarkowski, Edward J., ADP 50th Anniversary Book, Automatic Data Processing, Inc., 1999.

[3] http://www.adp.com/employer_services_overview.asp?iid=EFI0483

[4] Secord, Greg, VP of Marketing, ADP NAS, 30 March 2007 (verbal conversation)

[5] Secord, Greg, VP of Marketing, ADP NAS, 30 March 2007 (verbal conversation)

[6] ADP, 50th Anniversary : 1949 – 1999, p.5. p. 14

[7] Secord, Greg, VP of Marketing, ADP NAS, 30 March 2007 (verbal conversation)

[8] Automatic Data Processing, Inc. Company Profile, DataMonitor, p. 8.

[9] Automatic Data Processing, Inc. Company Profile, DataMonitor, p. 5.

[10] Secord, Greg, VP of Marketing, ADP NAS, 30 March 2007 (verbal conversation)

[11] ADP, Focus on growth : 2006 summary annual report, 2006. http://www.investquest.com/iq/a/adp/fin/annual/index.htm

[12] ADP, 50th Anniversary : 1949 – 1999, http://www.investquest.com/iq/a/adp/main/archives/anniversary.htm

[13] Automatic Data Processing, Inc. Company Profile, DataMonitor, p. 6.

[14] Automatic Data Processing, Inc. Company Profile, DataMonitor, p. 6

[15] ADP, 50th Anniversary : 1949 – 1999, p.5. p. 30., http://www.investquest.com/iq/a/adp/main/archives/anniversary.htm

[16] Rubel, Brian, Sales Executive, ADP NAS, 25 February 2007 (verbal conversation)

[17] Secord, Greg, VP of Marketing, ADP NAS, 30 March 2007 (verbal conversation)

[18] ADP, 50th Anniversary : 1949 – 1999, p.5. p. 30

[19] Paychex 2006 10k report……………………………..

[20]ADP, 50th Anniversary : 1949 – 1999, p.43 http://www.investquest.com/iq/a/adp/main/archives/anniversary.htm

[21] Rubel, Brian, Sales Executive, ADP NAS, 25 February 2007 (verbal conversation)

[22] Secord, Greg, VP of Marketing, ADP NAS, 30 March 2007 (verbal conversation)

[23] Automatic Data Processing, Inc. Company Profile, DataMonitor, p. 6

[24] http://www.investquest.com/iq/a/adp/main/archives/adp031406analyst.pdf

[25] http://www.investquest.com/iq/a/adp/main/archives/adp031406analyst.pdf

[26] http://www.adp.com/about_philosophy.asp#strengths

[27] Simon, Ellen “ADP chief looks at expansion, not acquisition” ASSOCIATED PRESS (7 March 2007)

[28] Gelfand, Andrew “ADP Seen Holding Off Competition With ProBusiness Buy” Dow Jones News Service (6 January 2003) :Factiva

[29] Kisiel, Ralph “Reynolds, ADP aim for European growth” Automotive News Europe Volume 11; Nbr 3 (6 February 2006) :Factiva

[30] Jackson, Kathy “Dealer software market is booming; Multibranding boosts demand for dealership management programs” Automotive News Europe, Volume 11; Number 21 (16 October 2006) :Factiva

[31] ADP Annual Financial Analyst Conference Call Presentation. March 22, 2007

[32] Taulli ,Tom “ADP Tries Getting Even Better” Motley Fool (November 2, 2006) Accessed 4/14/07 <http://www.fool.com/investing/general/2006/11/02/adp-tries-getting-even-better.aspx.

[33] http://www.adp.com/about_philosophy.asp, “OUR BUSINESS CULTURE”

[34] Automatic Data Processing, Inc. Company Profile, DataMonitor, p. 6

[35] http://www.adp.com/about_philosophy.asp, “ORGANIZATIONAL STRUCTURE”

[36] Automatic Data Processing, Inc. Annual Financial Analyst Conference, “Strategic Growth Program”, Slide 16, March 22, 2007

[37] Notes from meeting with ADP executive on 3/30/07

[38] ADP. (2007). 2006 Annual Report. Retrieved March 24th, 2007 from http://www.investquest.com/iq/a/adp/fin/annual/index.htm

[39] Gordon, Benjamin and Gordon, Matt, “The PEO Industry in Transition,” HRO Today, June 2006.

[40] Gluckman, Ron, “Shifting into High Gear,” The Silk Road, April 2004

[41] Lienert, Dan. “The Rising Chinese Auto Market,’Forbes.com, December 2003.

[42] Hemerling, Jim, Jin, David, and Chen, Forrest, “Winning in Today’s Chinese Automotive Market,” The Boston Consulting Group, June 2005

[43] ADP. (2007). ADP Press Release. “ADP Announces Major Contract With BMW China Automotive,” February 2007.