Introduction

The conventional wisdom with respect to Costco is that its business model forms a “defensive moat” against the conquering retail army of “House Bezos”. Costco offers its loyal shoppers a reason to visit its warehouses replete with low cost bulk items, pharmacies and food courts. This sentiment has held, but nothing drains a moat faster than when Amazon expands its physical retail presence into your market with a splashy $13.7 billion acquisition (see Whole Foods). We don’t quite know what Amazon is up to in the grocery sector (and meal kit delivery space), but given its track record of disruption, Costco better start taking up a stronger defensive position to enable long term success. At a minimum, we can expect Whole Foods to adopt best practices and leverage world-class data mining capabilities from the Amazonian fiefdom. The prevailing thought is that Amazon will revolutionize how groceries are purchased.

Unfortunately, Costco is a laggard in the technology investment arms race as compared to B2C heavyweights Amazon and Walmart; even as e-commerce has captured a larger share of sales industry wide. Costco’s main competitors are devoted to having formidable omni-channel presences which will drive future revenues. In the second quarter of 2017, Walmart’s e-commerce revenue grew 63%; even Target saw a 22% increase as compared to Costco’s 11% [1].

Amazingly, Costco consciously chooses to underinvest in its e-commerce capabilities, which I believe is a disservice to an otherwise strong business model (and the continuing availability of $4.99 rotisserie chickens). In an industry where market share is being gobbled up by a noted technology disruptor, it’s as if Costco has subscribed to the “IT Doesn’t Matter” philosophy. Costco is not only on the defensive technology wise, it’s in catch-up mode.

On June 15th, 2017 the day before Amazon’s Whole Foods acquisition was announced, Costco stock opened at $180.39. One day later the stock dropped 8.5% to close at $165. As of August 4th, 2017 the stock trades at $156.44 representing a 13.2% drop from June 15th. A more competitive grocery sector combined with Costco’s underwhelming investments in e-commerce technology have not inspired investors as of late.

In this post I’ll touch upon Costco’s advantages with respect to its competitors in the consumer staples and grocery sector, as well as offer some recommendations for its burgeoning digital strategy.

What Costco Does Well (Its Defensive Moat Against Competitors):

The “Treasure Hunt”

Let me be clear, Costco is not going anywhere in the medium run. Its revenues in 2016 totaled $119 billion as compared to $136 billion by Amazon. Costco’s value proposition relies upon attracting customers to its bricks and mortar warehouses, which are infused with “treasure hunt” and impulse purchase appeal. Shoppers explore the vast warehouses and stumble upon unexpected items, bargains and free samples that they didn’t know they wanted in the first place. The company believes that in-store customers will purchase many more items than they would otherwise purchase via an online channel.

Copyright: ultimagaina / 123RF Stock Photo

“We still are a bricks-and-mortar entity and we want to get you into the store because you’re going to buy more in the warehouse. You’re going to buy more when that happens, and we’ve got a lot of reasons for you to do that. We also recognize we don’t want to lose the sale to somebody else because they only buy online.” [2] – Costco CFO Richard Galanti

Because Costco sells many items in bulk, it is rightfully apprehensive of the freight costs associated with e-commerce. However, it needs to make progress in shoring up delivery capabilities if it wants to keep pace with Amazon and Walmart; potentially through investments in additional fulfillment centers. Walmart offers many bulk items online through Samsclub.com. Walmart is even experimenting with online order pickup at Sam’s Club locations.

“About a year ago, Costco CFO Richard Galanti said the only thing keeping him up at night is ‘everybody in the world never wanting to leave their house and only typing stuff to order and get it at the front door.’” [3]

Low Prices

In-store customers load up their baskets with groceries and other items in bulk with minimal price markups. Low prices are a strong competitive differentiator for Costco in that it has some of the lowest gross margins in its industry.

“Wal-Mart and Whole-Foods price their goods up higher. Wal-Mart posted 25.65% gross and 2.81% net margins in 2016. Whole Foods, known for its pricey merchandise, had 34.41% gross and 3.22% net.” [4]

Consider that Costco’s numbers are razor thin gross margins of 13.32% and net margins of 1.98%. The bottom line is that Costco shoppers obtain industry leading pricing from the company’s warehouses. Costco appeals to a wide variety of shoppers and it even attracts business customers looking to buy in bulk. In contrast, Whole Foods (derisively known as Whole Paycheck) appeals to a higher income demographic in search of artisanal offerings; thus there is minimal overlap with Costco’s broader range of shoppers. However, Amazon Prime members and Costco members overlap as both customer bases are in search of low prices.

Further enabling Costco’s low price scheme is its strategic use of vertical integration for enhancing product quality and increasing profitability. “Such integration includes Costco working with farmers to help them buy land and equipment to grow organics, building its own poultry farm, owning and operating its own beef plant and hot dog factory, and having its own optical grinding factory.” [5]

Memberships

Costco makes most of its money from selling memberships. The company is able to offer such low pricing and still make a profit because of its successful membership model. Costco charges $60 for its standard memberships and $120 for its executive memberships which pay-out a 2% redeemable award on pre-tax purchase amounts.

“Our membership format is an integral part of our business model and has a significant effect on our profitability. This format is designed to reinforce member loyalty and provide continuing fee revenue. The extent to which we achieve growth in our membership base, increase penetration of our Executive members, and sustain high renewal rates, materially influences our profitability.” [6] – Costco 2016 10K Filing

In other words, it’s easy to match or beat competitor pricing when your business model is buoyed by piles of membership cash. Costco’s 88 million memberships worldwide represent a healthy revenue stream for the company, accounting for an astounding 72% of pretax profits [7]. Furthermore, Costco shoppers renew their memberships at a high rate (roughly 91% in the U.S. and Canada and 88% on a worldwide basis). However, Costco would be wise to note that its “membership revenue growth has decelerated to around 5.5% from around 7%” [8].

Kirkland Signature: The Private Label Brand Everyone Loves

Copyright: deanpictures / 123RF Stock Photo

Whether you are a Costco member or not, you are most likely familiar with its “Kirkland Signature” in-house brand which was started in 1992. The successful brand sells everything from dress shirts to luggage to vodka (i.e. the consultant staples). Costco has done a first-rate job of making Kirkland Signature a strong value play alternative to national brands.

“‘Costco’s Kirkland Signature is the best store brand there ever was,’ said one writer at foodie bible Bon Appetit in August, the same month Wal-Mart paid $3.3 billion for Jet. ‘You wouldn’t expect a brand that makes cashmere sweaters, batteries, and 900-count packs of baby wipes to also produce some top-notch food products’” [8]

Sales of individual Kirkland items have been reported to exceed $1 billion and the brand itself constitutes roughly 25% of Costco’s revenue. Although Amazon’s Whole Foods carries a “365” private label brand and Walmart carries “Sam’s Choice” and “Member’s Mark” (amongst others), both competitors offer Costco’s Kirkland Signature brand through their e-commerce properties.

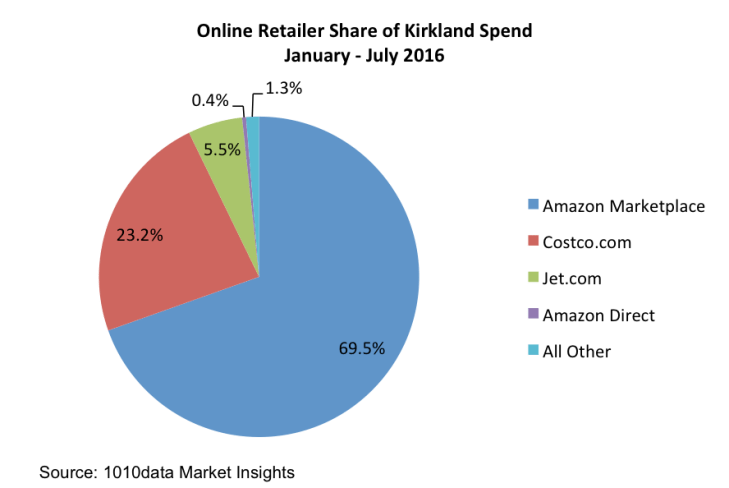

According to research from 1010data Market Insights, 69.5% of Kirkland online spend [9] is generated on Amazon! This unofficial cross-platform selling indicates a mashup between strong brand preference and the number one retail e-commerce portal. Since the current selection of Kirkland Signature branded products available on Amazon is offered by third parties, there is an opportunity to capture a portion of that online demand through the official Costo.com channel. Jet.com (recently purchased by Walmart for $3.3 billion) has indicated a phase out of Costco products in order to boost the popularity of the Sam’s Club “Member’s Mark” private label.

Recommendations for Costco:

I’ll open this section with Costco’s own words from its 2016 Annual Statement:

“If we do not successfully develop and maintain a relevant multichannel experience for our members, our results of operations could be adversely impacted. Multichannel retailing is rapidly evolving and we must keep pace with changing member expectations and new developments by our competitors.” [6]

Costco’s relative lack of ambition in e-commerce capabilities leaves the company vulnerable to disruption. Its online sales are currently $4 billion or barely 3% of sales; this figure is far less than smaller revenue retail players like Best Buy and Macy’s [10]. Walmart has poured billions of dollars into its digital and e-commerce capabilities in order to keep pace with Amazon. Costco would do well to leverage some items from the Walmart playbook.

-

- Invest in an e-commerce research division to help bolster the organization’s base expertise in this space. Acquire the necessary pool of data scientists, software engineers and PhDs to inject new life into a digital and technology focused strategy.

-

-

- This approach will allow the company to increase its capabilities in e-commerce basics such as search functionality, order tracking and predictive analytics. Costco is already located in the technology rich talent pool known as greater Seattle.

-

-

- Offer more items online at Costco.com. Focus on re-capturing some of the demand for Kirkland branded Costco products from Amazon. It bears repeating that 69.5% of Kirkland online spend is generated on Amazon!

-

- Acquire startups to gain access to digitally focused management teams and their respective technology and insights (a la Walmart’s purchase of Jet.com and Marc Lore). Internal disruptors help cross-pollinate successful ideas that are not considered by the core legacy business.

-

-

- In this sense Costco should acquire Chieh Huang’s e-commerce warehouse startup “Boxed”. Boxed was started in 2013 out of the founder’s garage and is currently known as the “warehouse in your pocket” by millennials. Boxed enables bulk goods to be ordered directly from a mobile app without the need for membership fees.

- Currently Boxed offers free deliveries on orders of $49 or more. Although Boxed delivers non food items in bulk, it currently purchases its food items from Costco and marks up the price for delivery! [11] Costco has an opportunity to acquire a startup rival in order to gain access to its e-commerce talent.

-

-

- Install drive through stations where customers can pick up online orders at either Costco warehouses or dedicated “click and collect” facilities. Walmart’s Sam’s Club currently offers this service at about 65 of its 660 US stores [12]. The company should be aware that members will not want to pay the markup associated with delivery specialists Instacart and Google Express; especially Costco members who have shelled out for a yearly membership.

-

- Increase investments in fulfillment centers that will help temper the expenses associated with shipping bulk products ordered online.

-

- Get better at the basics with respect to information technology infrastructure. Granted, core IT infrastructure is not necessarily a strategic resource but it is the cost of doing business. Consider this quote from Costco CEO Richard Galanti:

-

-

- “You know, about three-and-a-half years ago, when we embarked on this dark journey, [we recognised that] we probably had the lowest-cost IT out there. I always joke we were in the greatest MASH unit. It was always up and running, but band-aided to death.” [2]

-

Costco needs to realize that its “treasure hunt” appeal to customers needs to be paired with a more robust omni-channel approach. This means Costco must ramp up its capital expenditures in e-commerce and mobile just to keep from losing pace with industry competitors who have a substantial head start. Costco will be fine in the medium run for all the reasons I’ve highlighted earlier. But how long until continued e-commerce disruption crosses the organization’s defensive moat and treats Costco like one of its mouthwatering rotisserie chickens?

For more retail related technology coverage check out:

- The Definitive Walmart E-Commerce and Digital Strategy Post

- More Than You Want to Know About Walmart’s Technology Strategy Part 1

- More Than You Want to Know About Walmart’s Technology Strategy Part 2

- More Than You Want to Know About Walmart’s Technology Strategy Part 3

References:

[1] Sozzi, B. Jul 19, 2017. Here Is What Costco Should Do to Keep Amazon From Being the Largest Company on Earth. https://www.thestreet.com/story/14233036/1/here-are-the-big-things-costco-could-do-to-keep-amazon-from-being-the-largest-company-on-earth.html

[2] Lauchlan, S. March 8 2017. Costco – an e-commerce tortoise takes on the omni-channel hares. http://diginomica.com/2017/03/08/costco-e-commerce-tortoise-takes-omni-channel-hares/

[3] Levy, A. March 12, 2017. Not Even Costco Is Safe From Amazon. https://www.fool.com/investing/2017/03/12/not-even-costco-is-safe-from-amazon.aspx

[4] GuruFocus. June 22, 2017. After Amazon’s Whole Foods Acquisition, Investors Are Looking At Costco. https://www.forbes.com/sites/gurufocus/2017/06/22/after-amazons-whole-foods-acquisition-investors-are-looking-at-costco/#18b01a50271d

[5] Tu, J. June 19, 2017. Amazon’s move into groceries could squeeze Costco. http://www.seattletimes.com/business/retail/amazons-move-into-groceries-could-squeeze-costco/

[6] Costco Wholesale Corp. 10K/A Annual Report for the Fiscal Year Ending Sunday August 28, 2016. https://www.last10k.com/sec-filings/cost/0000909832-16-000034.htm#

[7] Fonda, D. July 2017. Costco Is Surviving in the Age of Amazon. Warehouse giant Costco continues to prosper despite the growth of internet retailing. http://www.kiplinger.com/article/investing/T052-C008-S002-costco-is-surviving-in-the-age-of-amazon.html

[8] Boyle, M. June 12, 2017. Jet.com Will Phase Out Costco Products After Wal-Mart Acquisition. https://www.bloomberg.com/news/articles/2017-06-12/wal-mart-s-jet-com-carries-costco-products-but-not-for-long

[9] Wilson, T. September 13, 2016. Kirkland’s Online Enterprise. https://1010data.com/company/blog/kirkland-s-online-enterprise/

[10] Wahba, P. December 8,2016. Costco’s Battle Plan for the E-Commerce Wars. http://fortune.com/2016/12/08/costco-ecommerce/

[11] Fickenscher, L. August 4, 2017. Boxed buys from rival Costco before hiking prices for delivery. http://nypost.com/2017/08/04/boxed-buys-from-rival-costco-before-hiking-prices-for-delivery/

[12] Young, J. April 5, 2017. Why Costco Loves Store Sales: You Try Shipping a Tub of Mayo http://www.foxbusiness.com/features/2017/04/05/why-costco-loves-store-sales-try-shipping-tub-mayo.html

Header Imagine: Copyright: niloo138 / 123RF Stock Photo

hi thanks for the information

LikeLike

Great post

LikeLike

Great Post

LikeLike